When a Disaster Strikes:

What to Do After an Insured Homeowners Loss

A Question and Answer Guide for Homeowners

Prepared by

Commonwealth of Virginia

State Corporation Commission

Bureau of Insurance

This Consumer's Guide should be used for educational purposes only. It is not intended to be an opinion, legal or otherwise, of the State Corporation Commission on the availability of coverage under a specific insurance policy or contract, nor should it be construed as an endorsement of any product, service, person, or organization mentioned in this guide.

2018-2021

Commonwealth of Virginia

State Corporation Commission

P.O. Box 1157

Richmond, VA 23218

Bureau of Insurance Landing Page

How do I report a claim?

Your insurance agent is the first link between you and your company. If your agent is unavailable or if your insurance company does not have representatives on the scene available to help you, call the company directly and ask for the claims department. The company's phone number is listed in your policy or can be obtained through the Bureau of Insurance. Your insurer’s website may provide important information on how to report a claim.

It is very important that you fully understand your rights and responsibilities so that you can take charge of your own situation. If your insurance policy has been lost or destroyed in the disaster or if you are confused about the policy benefits or exclusions, your agent or company will be able to tell you exactly what coverages you have purchased. Remember that some disaster- related losses are not covered under your policy. For example, standard homeowners policies do not cover flood damage. This guide contains additional information regarding damage due to floods.

What should I do if my company has not responded to my claim?

After you report your loss, the insurance company will assign a company representative to check the damage to your property and determine how much will be paid for your loss. If it is necessary to vacate your home, be sure to report the address and phone number where you can be reached.

Virginia has certain laws and regulations that govern the claims handling practices of your insurance company. For example, insurance companies are required to acknowledge the receipt of your claim within 10 working days. They are also required to provide you with the appropriate forms to file a claim. If your company has not responded to you within the required period of time or if you have experienced any other unreasonable delays in the handling of your claim, the Bureau of Insurance can provide assistance.

What information must I give to the company representative?

Your homeowners policy requires you to complete a claim report which lists all items destroyed, damaged, or missing. If you do not have or cannot locate a complete household inventory, try to picture the contents of every room in your home, and then list and describe all the items that were damaged or destroyed. Include furniture, major appliances, electronic equipment, and pictures or accessories in each room. Be sure to include hobby items such as fishing or camping equipment, tools, and other home maintenance items and seasonal items such as holiday decorations or outdoor furniture.

As accurately as possible, try to remember when or where you bought each item, how much you paid for it, and how much it will cost to replace it. It is also helpful to include the brand name and model number if you know it.

What services can I expect from the company representative?

The representative may ask to examine all damaged items to prepare a written damage estimate for the company. You may ask for a copy of this report and should not hesitate to ask questions if you do not understand it or need help in completing the claim form.

Should I wait for the company's permission to begin clean-up?

To protect your property from further damage, you should make all necessary temporary repairs, such as boarding up windows and patching holes in walls or roofs, as soon as possible, even if you have not yet seen the company representative. You can also move your personal property to a protected area and begin cleaning and drying items damaged by water. However, you should not dispose of any items that you believe may be a complete loss until the company representative has examined them.

Take photographs to show the way things look before you begin cleaning and repairing, and be sure to keep receipts for all of your clean-up expenses. Most homeowners policies cover the reasonable costs of emergency clean-up and temporary repairs.

Can I hire someone to make emergency repairs?

Probably. Most homeowners policies cover materials and reasonable labor expenses for temporary and emergency repairs in addition to any final repairs made to your property. You should also ask your company representative whether the company will compensate you for work you do yourself. Be sure to keep all of the receipts.

How should I go about choosing a contractor to make repairs?

When choosing a contractor, you should make sure that you deal only with established firms or individuals who can provide references and are willing to give you a signed contract. If family members or friends cannot recommend a reputable contractor, check with the local disaster center, your local building code department, or the Better Business Bureau for guidance.

Obtain written estimates before repairs begin, and do not sign any contracts for major repair until the company representative has determined how much damage there is and how much the company will pay.

A contractor told me he can do the job faster if I just sign my check over to him. Is that a good idea?

No. If the repair work is extensive, the contractor may ask for periodic partial payments as the work progresses, but it is highly unlikely that a reputable contractor would request full payment in advance. The contract should specify that payments will be made as the work is completed. If you have a mortgage on your home, the lending institution may also have specific requirements as to how the insurance funds are disbursed.

What if my contractor says the repairs will cost a lot more than the company representative has allowed?

If there is a discrepancy over the cost of repairs or the contractor has found hidden damage, contact the company representative to try to resolve the difference. If you are still unable to resolve your differences, contact the Bureau of Insurance.

Where can I live while my house is being repaired?

If you have purchased a homeowners insurance policy and your policy provides coverage for your loss, you will be insured for "Additional Living Expense" coverage, which pays for costs you incur that are in excess of your normal living expenses. For example, if you normally spend $1500 per month for mortgage/rent, utilities, food, and transportation, and these living expenses increase to $2,000 per month because of the disaster, the insurance company will reimburse you $500. Be sure to save all receipts.

You should also ask your company representative if there are any restrictions on where and how long you can stay and how much you are allowed for hotel rooms. If you stay with a relative or friend, the company may reimburse your host for lodging only if you can show proof of actual payment. Extra expenses, such as higher utility bills, incurred by the host would definitely be considered. You can also submit a claim for the cost of storing your personal property until your home is ready for occupancy.

How much will the company pay to repair/rebuild my home?

If you have purchased a replacement cost policy and have met the company's "insurance to value" requirements, there are different ways the company may pay replacement cost. The most usual way is for the insurer to make a partial payment (ACV) until the property has been repaired. You have six months to make a claim for the difference between the ACV and the full cost of repairs, up to the policy limits, using similar construction. Once the property has been repaired, the insurer will pay this difference.

If you elect not to repair the building, you can submit a claim for the actual cash value of the damaged building. You then have six months from the date of the actual cash value payment or the date of a final judgment, whichever occurs last, to make a replacement cost claim.

Will my homeowners policy cover the costs of meeting local/state building codes and ordinances when I repair or rebuild my home?

First, check with your agent to determine whether your policy includes a building code endorsement that will pay these expenses. In most cases, however, homeowners policies do not cover the expense of bringing a house up to code or meeting certain ordinances (including flood plan requirements) if the house did not meet these requirements when it was destroyed. Your company is required by Virginia law to offer you the option of buying this coverage.

If your policy does not cover these costs or if you did not buy the additional coverage, check with the federal agencies at the local disaster center to see if you are eligible for any financial assistance.

What about my household contents and other personal property?

Again, it depends on the type of policy you purchased. Insurance policies pay either on an actual cash value basis or on a replacement cost basis. Be sure to check with your agent or insurer if you are not sure what coverage you purchased.

Actual cash value is the amount equal to what the items were actually worth at the time they were damaged or destroyed. For example, it might cost $1,000 to replace your sofa at today’s prices. If the average useful life of a sofa is 20 years, and your sofa was 10 years old on the day it was destroyed, the company would pay you $500.

If you paid for replacement cost coverage, the company may first pay you the actual cash value as described above. Once you have actually replaced the items and submitted your receipts, the company will then pay you the difference. Using the above example, the company would initially pay you only $500 for your damaged sofa. After you buy the new one for $1000, the company would then reimburse you another $500 - the difference between the actual cash value and the replacement cost. Some companies also use replacement services that will obtain certain items such as appliances for you. Policy provisions vary, so you should check with your agent or your company to find out the specific requirements for this coverage.

As you begin replacing damaged items, be sure to keep all receipts. It may be advisable to submit accumulated receipts to the company every two weeks or so rather than sending them in one at a time. If you elect not to replace the damaged items, you can submit a claim for the actual cash value of those items. You then have six months from the date of the actual cash value payment or the date of a final judgment, whichever occurs last, to make a replacement cost claim.

Is my company obligated to pay for my antique furniture and expensive jewelry?

Not necessarily. Most homeowners policies place specific dollar limits on items such as jewelry and will only pay the actual cash value of antiques (which may or may not be equal to their appraised prices). You must purchase additional coverage to insure these items in full. If you have not done so, they may not be fully covered on your regular homeowners policy.

I may have forgotten to include some items in my claim. What should I do?

If you forgot to list some items when making your claim, contact the insurance company. Unless the company has paid the entire limit for the coverage on those items, it is not unusual for the insurance company to make an additional payment. However, it is important that you file an accurate claim in a timely fashion.

The damages to my house will cost a lot more than the insurance policy covers. What can I do?

Check with the federal agencies at the local disaster center to see if you are eligible for a grant or low-interest loan.

How will the company pay me?

Your policy divides your claim into two separate parts - one for the house itself and one for the personal property or contents. You may also be entitled to reimbursement for additional living expenses. The check or draft for payment for the contents claim will be made out to you. However, the check or draft for the house may be payable to you and your mortgage holder if there is a mortgage on your house.

Chances are, you received an advance check immediately after the disaster to cover such items as additional living expenses and clothing. It is important that you keep receipts for all items purchased with this money because when the claim is finally settled, any amounts previously paid will be deducted from the final check.

Will my homeowners policy pay for flood damage to my home?

Standard homeowners policies do not cover flood damage. However, if you have a flood insurance policy, your company or the National Flood Insurance Program will assign an adjuster to handle your claim.

If your home is not covered for flood damage, you should check with the federal agencies at the local disaster center to see if you are eligible for federal assistance, including grants or low-interest loans.

Will my homeowners policy pay for earthquake damage to my home?

If you do not have earthquake coverage, any structural damage attributed to the quake would not be covered. Most insurers allow the insured to purchase earthquake coverage, and a few insurers offer a homeowners policy that includes some earthquake coverage. Your agent or insurance company representative can advise you if your policy includes coverage for damages caused by earthquakes and can explain the deductible, which is typically a percentage of the amount of insurance on your dwelling.

If you do not have earthquake coverage, you should check with the federal agencies at the local disaster center to see if you are eligible for financial assistance.

Will my homeowners policy pay for mine subsidence damage to my home?

Most homeowners policies do not cover damage due to mine subsidence.

My homeowners policy has a separate deductible applicable to hurricane losses. How does this work?

Some homeowners policies contain a special deductible for wind or hurricane losses. These deductibles are applied separately from any other deductible on the homeowners policy. Some companies automatically include a wind or hurricane deductible, while other companies make this deductible available at the option of the policyholder. Some wind or hurricane deductibles are written as a flat amount, such as $1,000, while others are applied to the loss as a percentage of the insurance coverage on the dwelling. For example, assume a hurricane causes damage to your house amounting to $3,000, and your dwelling is insured for $100,000. If your policy has a 2% hurricane deductible, the deductible would be $2,000, and the company would pay $1,000.

What about damage to my automobile?

Your car is not covered under your homeowners policy. If you have the appropriate comprehensive or collision coverages, the company should reimburse you for damage to your car just like any other auto claim. Check with your insurance agent.

If a tree falls in my yard but does not damage my home or property, will insurance pay for clean up and removal?

Generally, the fallen tree must cause damage to your home or property before the insurance company is obligated to pay for clean up and removal. However, some policies provide limited coverage for clean up and removal of trees – for example, trees that fall and block your driveway.

If a neighbor's tree falls on my property and hits my home, should my neighbor's insurance company pay?

Unless negligence can be proven, the neighbor’s policy covers his/her house, and your policy covers your house. Generally, if the tree is damaged due to a storm, the owner would not be considered negligent.

There was no damage to my home, but $400 worth of food was lost because of the power outage. Can I file a claim for the loss?

You should contact your agent or insurance company or read your policy to see whether you have coverage for food spoilage because not all policies provide coverage for food spoilage.

My tree fell on my house or on my fence or on my deck furniture. Will the company pay for the cost to remove the tree?

Most policies pay for the reasonable cost for clean up and removal of trees that fall and cause damage to your fence or deck furniture.

My tree is hanging over my house. It hasn't fallen, but it is posing a danger to the property and my family. Will the company pay for the cost to remove the tree?

Most policies do not provide coverage for removing trees that may fall on the property.

A tree is on my roof. Will the company pay for me to have the roof tarped?

Insurers expect homeowners to protect their property from further damage and will pay the reasonable costs associated with protecting the property. Contact your agent or insurer immediately to discuss temporary repairs and the steps you should take to mitigate your damages. Some fire departments may be able to assist you. Whenever you make temporary repairs, be sure you save all damaged property for the adjuster to inspect. Placing tarps on the roof is a way of protecting your property from further damage.

What am I supposed to do when the company won't come to the house for at least a week and rain is predicted? Can I get a contractor to start repairs?

Most insurance companies will want to see the damage before final repairs are made. If you have to make temporary repairs, you need to take pictures of the damaged property before making any temporary repairs, and keep receipts of what you’ve spent. Unless the insurance company has advised you in writing to go ahead and make final repairs, you should wait.

I have a hurricane deductible. I have wind damage. Is that considered a hurricane?

It is important to read the policy to see how the deductible is described.

Is there a difference between a hurricane and a wind deductible?

It depends on how the policy describes the deductible. Yes, there is often a difference between wind deductibles and hurricane deductibles. Hurricane deductibles are more specific. Wind deductibles can be triggered by a thunderstorm, tropical storm, or a hurricane.

Does the wind deductible apply to the entire loss (i.e., additional coverage like debris removal and food spoilage) or just my home?

It depends on how the policy describes the deductibles. It is possible that more than one deductible will apply. There could be a wind deductible that applies only to buildings and another deductible that applies to debris removal or food spoilage.

What do I need to do to prove that the loss occurred? I need to clear the area of debris and throw out spoiled food and can't wait indefinitely for the claim adjuster to inspect the property.

Take pictures, record your damage, keep a list of expenses, and keep a list of any discarded items. It is reasonable to remove debris that prevents access to your driveway or home.

Will my policy pay for me to stay in a hotel if my power is off and I have no water?

Most policies pay for the extra expenses of staying in a hotel or eating out only when your home is uninhabitable – basically when it is unsafe to continue to live there.

Will my policy pay for a generator?

Generally, no. However, you may wish to contact your agent or insurer to determine if your specific circumstances would allow an insurer to reimburse you for this expense.

My neighbor's company paid him for spoiled food, but my company won't. Don’t all policies have food spoilage endorsements?

No, all policies do not cover food spoilage.

My house was destroyed by the storm, and I had a fuse box that the city says doesn't meet code. Will my policy pay to replace the fuse box with a circuit breaker system?

Although most policies do not cover the cost of upgrading the property to meet the building codes, this coverage is available for an additional charge.

Does my homeowners policy provide property coverage for damage to my boat?

Most homeowners policies provide a small amount of property coverage for watercraft. The amount of coverage may vary, but $1,000 is typical. Since watercraft is “personal property,” the causes of loss and exclusions applicable to personal property or contents apply. It is important to note that watercraft (except row boats and canoes) is NOT covered for windstorm or hail unless the property is inside a fully enclosed building. A homeowners policy may be written or endorsed to include more coverage.

Boat or watercraft policies vary, so it would be necessary to review each policy to determine the applicable coverage.

What should I do if I have a loss?

-

You should contact your agent or insurance company as soon as possible.

-

Protect the property from further damage. Keep receipts from any expenses you incur from protecting the property or making temporary repairs.

-

Keep an inventory of your damaged property – take pictures or video the damage if possible.

Who should I call to report a claim if I have flood insurance?

Contact the National Flood Insurance Program (NFIP) if your policy was written directly with the NFIP. Their toll free number is (800) 638-6620.

Also the NFIP’s website www.floodsmart.gov contains information on how to file a claim, news alerts, and important information on the flood policy.

Most policies are written by participating insurers. If your policy was written by one of the participating insurers, contact that insurer or your agent to report the claim. If you can’t locate your policy information or need help contacting your insurance company, call (800) 427-4661 to talk to an NFIP specialist.

Can the Bureau assist me if I have a problem with my flood insurance claim?

Because flood policies, whether written by an insurance company or directly with the National Flood Insurance Plan, are administered by the federal government, the Bureau of Insurance is only able to provide limited assistance.

What Should I Do If I Have a Problem?

-

Contact your agent or company.

If you believe your insurance company has improperly cancelled or non-renewed your policy or has refused to pay all or part of a valid claim, you have a right to question and complain. Sometimes a mistake has been made, and it will be corrected if an inquiry is made. A complaint by letter is best. Keep a copy of your letter. If you decide to complain by telephone, keep a written record of:

-

The date and time of your call

-

The name of the person you talked to

-

What was said during the call

-

-

Seek help from the Bureau of Insurance.

If you do not receive a prompt, courteous, and satisfactory response, you may need to get help to resolve your problem.

The State Corporation Commission Bureau of Insurance provides free professional information and complaint services to all Virginia residents.

To use these services you can:

-

Call (804) 371-9185 if you live in Richmond.

-

Call toll free at (877) 310-6560.

-

Fax (804) 371-9349.

-

Call (804) 371-9206 for Telecommunications Device for the Deaf.

-

Review the Bureau's Website: Bureau of Insurance Landing Page

-

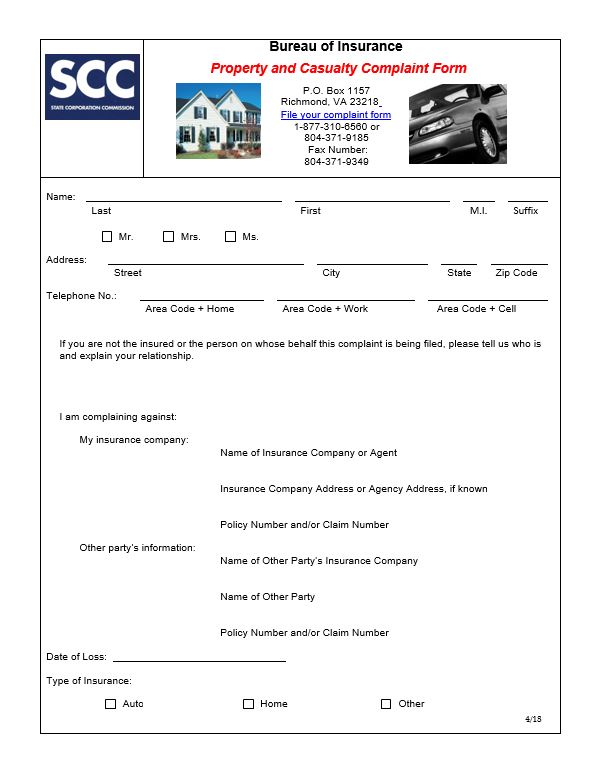

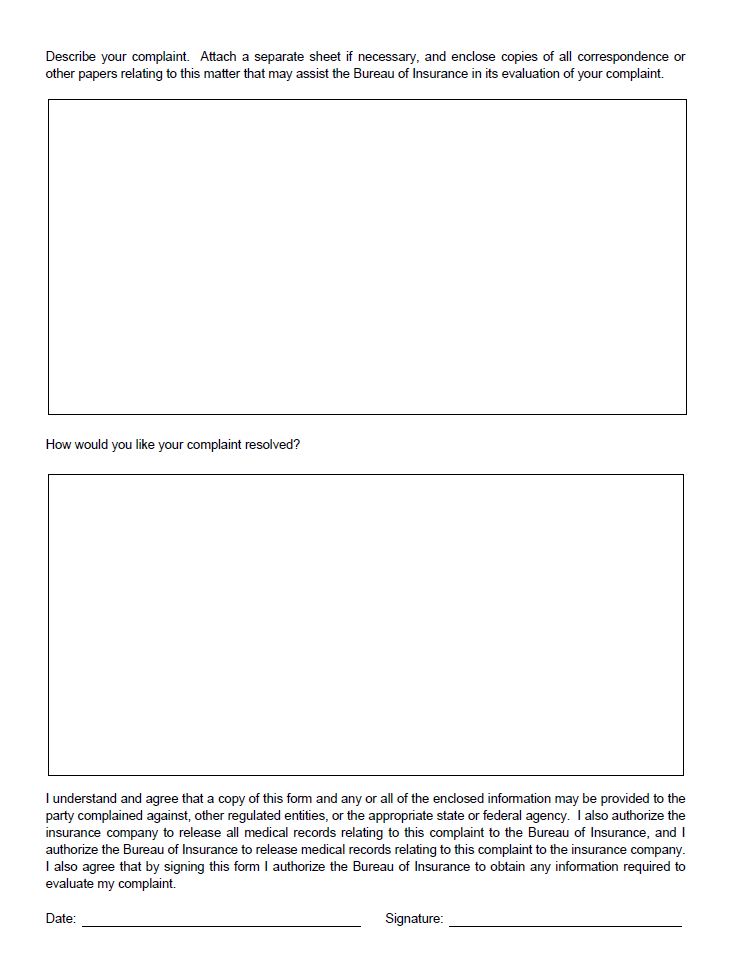

Use the complaint form at the bottom of this page or fill in and print this one and mail it to:

State Corporation Commission

Bureau of Insurance

P.O. Box 1157

Richmond, Virginia 23218 -

Visit the Bureau of Insurance

Tyler Building, 5th Floor

1300 East Main Street

Richmond, Virginia -

If you want to e-mail us with a general question, please contact us at: bureauofinsurance@scc.virginia.gov

-

The Bureau of Insurance will:

-

Thoroughly investigate your complaint;

-

See that you get a clear response to your questions;

-

Cut through red tape; and

-

Correct misunderstandings.

But the Bureau cannot:

-

Force a favorable action on your complaint if it is not supported by facts and law.

-

Provide legal services that are sometimes required to settle complicated problems.

If the Bureau is unable to resolve your problem, we will tell you why. If the law and facts are on your side, we will try to see that your rights are protected and that your complaint is resolved in a satisfactory manner.

Complaint Form